Mapping De-Dollarization Risk

The best risk maps are the ones nobody wanted to look at — until the fire started.

This de-dollarization framework was built before the Iran war kicked off — before Hormuz risk jumped from scenario planning into live pricing, before Gulf realignment went from theoretical to operational. It was a structural risk map. Now it's the baseline for counting the damage.

Most Western commentary treats de-dollarization as something that happens to other people — emerging markets, sanctions targets, the commodity periphery. The data says the opposite. The US is one of the most exposed nodes because the dollar system is so concentrated in US rails, US legal venues, US reserve demand, and US asset markets. Slow fragmentation makes that concentration look like strength. Shock fragmentation makes it a single point of failure at civilizational scale.

Here's the full working — built in Zorora, exported as a reproducible scoring script with visuals. Every line of logic is exposed. Pull it apart, run it yourself, break it if you can.

What You Need

The framework rests on three layers of evidence:

- a five-dimension geography model: currency denomination, clearing dependence, trade-system dependence, reserve vulnerability, and legal-framework exposure

- an asset-class ranking showing where de-dollarization reprices first

- an investor/owner map showing who is actually holding the most exposed balance sheets

The war overlay comes later. First you need the baseline.

Step 0: Start With Ordinal Risk, Not False Precision

The source framework is qualitative on purpose. It uses labels like Very High, High, and Moderate-High because the underlying phenomena are structural and multi-causal, not cleanly reducible to one econometric coefficient.

To plot it, we convert the labels into numerical scores — ranks, not probabilities:

RISK_SCORE = {

"Most exposed": 5.0,

"Very High": 4.5,

"High": 4.0,

"Moderate-High": 3.0,

"Moderate": 2.0,

"Low-Moderate": 1.0,

"Low": 0.4,

"Low (forced adaptation)": 0.6,

}

def risk_to_score(label: str) -> float:

return RISK_SCORE[label]Same judgment, now visible as a gradient. The chart doesn't claim Very High is 12.5 percent worse than High — it renders the hierarchy without inventing precision that doesn't exist.

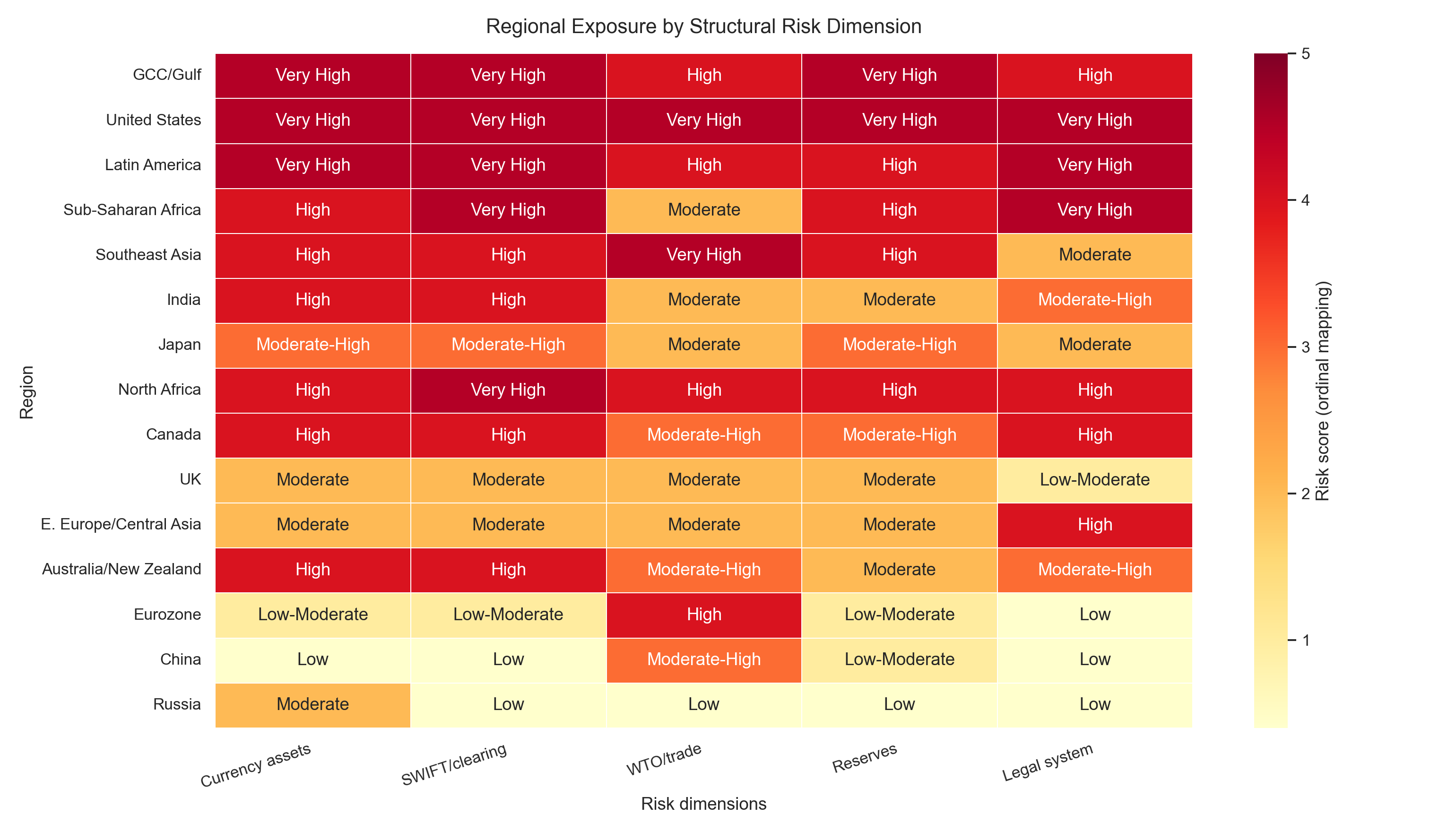

Step 1: Score the Regions Across the Five Channels

This is the structural layer. Each region scored independently across five channels, then given a composite label. The rows that matter most. Two things become obvious immediately.

First, the GCC is not just another rich allocator. It is the region where petrodollar plumbing, currency pegs, reserve exposure, and legal dependence stack on top of each other. Second, the US belongs inside the map, not outside it. If the framework is truly about exposure to dollar-system fracture, the owner of the system is not exempt from that fracture.

US and GCC at the same end of the map for opposite reasons — one owns the system, the other is hardwired into it.

This is where the state-motivation layer starts to matter. The GCC recycles dollar surpluses into US assets because the security architecture makes that rational. China builds alternative settlement rails because concentration in US rails is an obvious strategic vulnerability. Europe hedges rather than ruptures because its institutions still benefit from the incumbent order. Russia's low score is not resilience. It is post-2022 forced adaptation after paying an enormous price to disconnect.

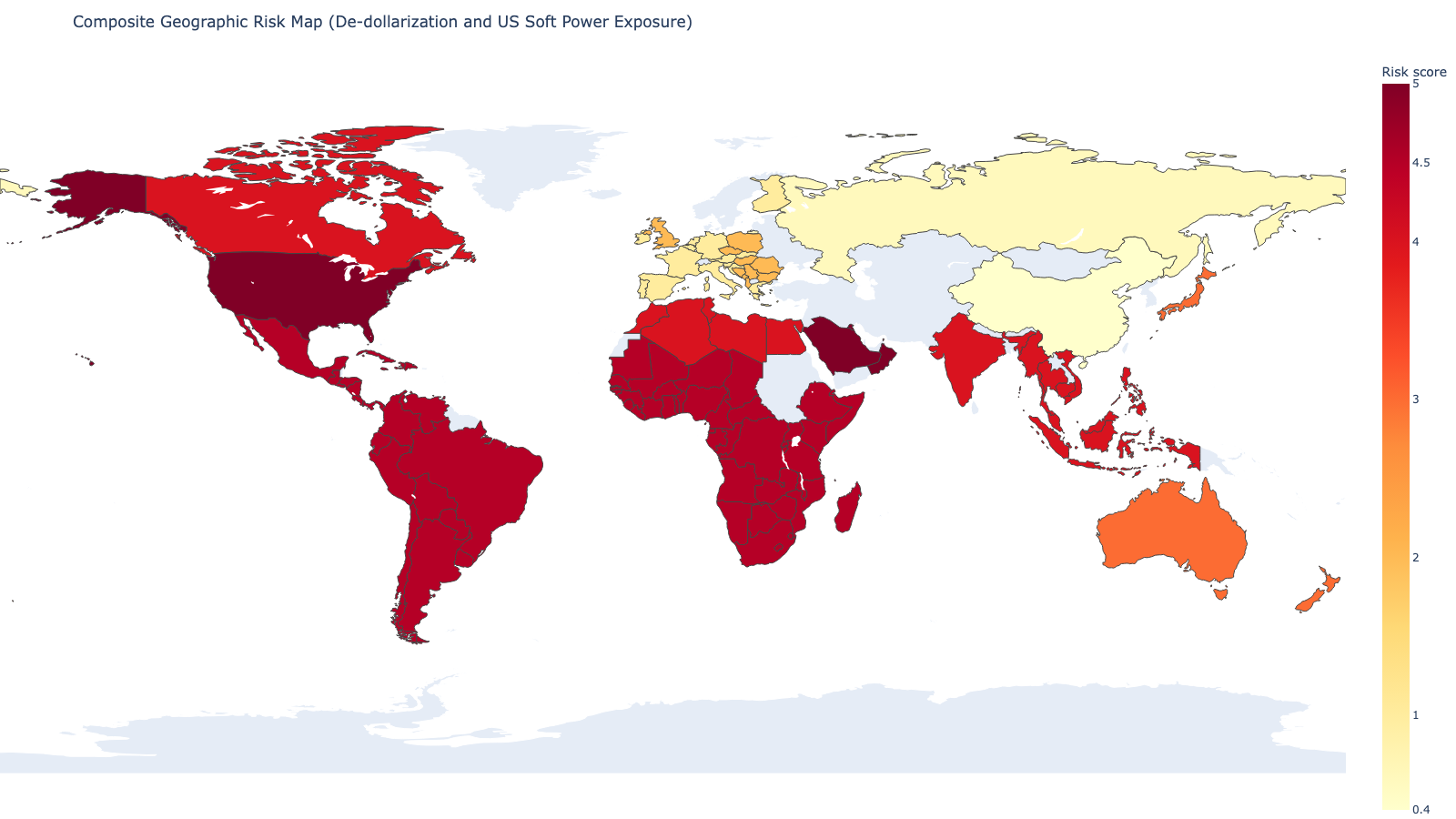

Step 2: Project the Scores Onto the World Map

Once the regional rows exist, the mapping logic is simple: assign countries to the framework regions, then color them by the composite score.

Not a prediction market. A topology of where balance-sheet stress already lives before anything triggers.

Red zones don't all break the same way — but dollar-system concentration isn't a peripheral problem. It sits dead centre in the US-GCC core.

That's the pre-war insight. If a security rupture makes Gulf dollar recycling politically untenable, the damage doesn't stay in the Gulf. It hits the US through the very channels the map flags as most concentrated: reserve demand, capital markets, legal-financial infrastructure, and the commodity system built around them.

Step 3: Do the Load-Bearing Capital Math

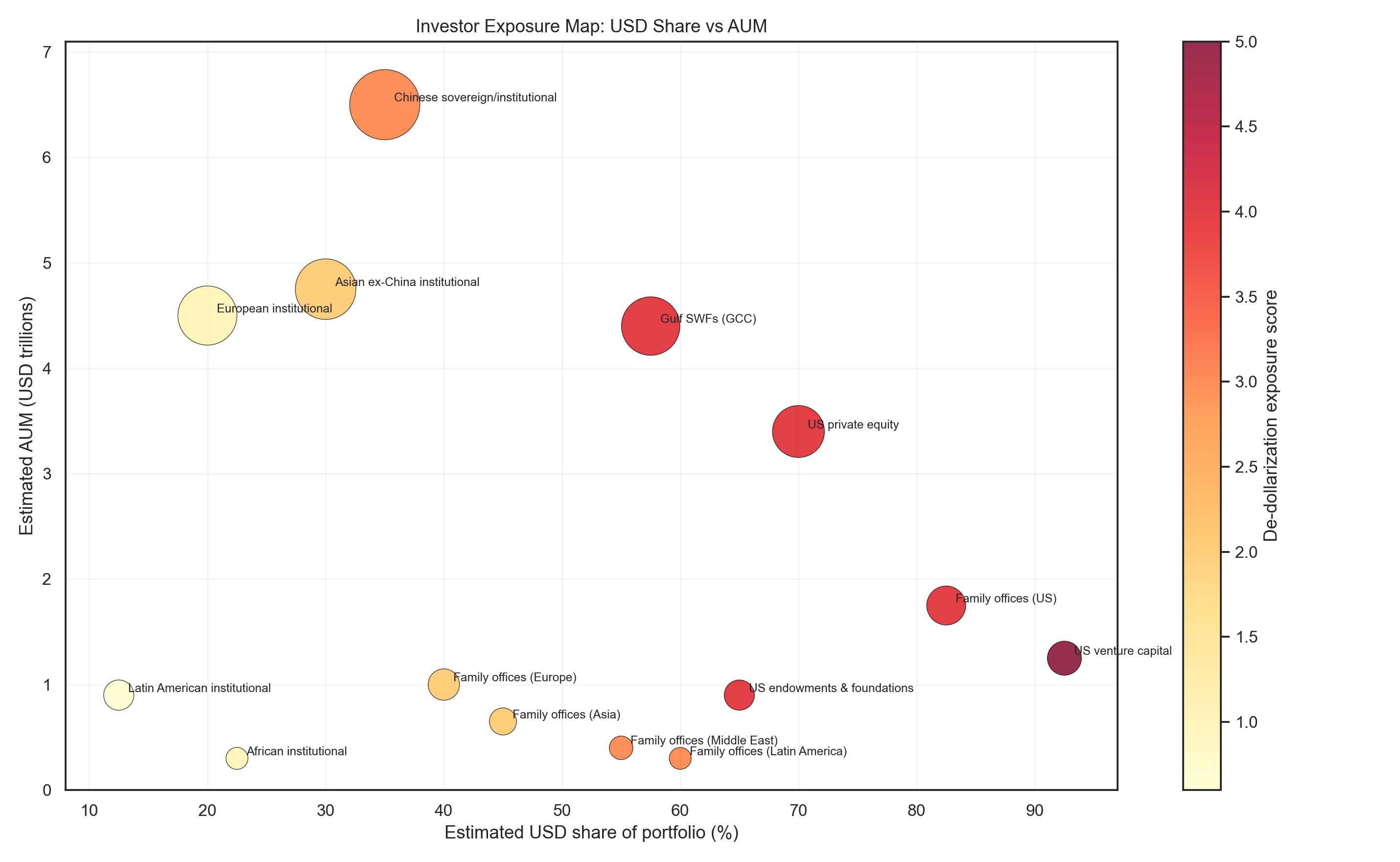

The framework only becomes politically meaningful once you connect it to actual owners.

The key number in the investor table is Gulf sovereign wealth exposure: roughly $4.0-4.8T in AUM with 50-65% effective USD share. That is not symbolic money. It is system money.

gcc_swf_aum_mid = (4.0 + 4.8) / 2

gcc_usd_share_mid = (0.50 + 0.65) / 2

gcc_usd_exposure_mid = gcc_swf_aum_mid * gcc_usd_share_mid

treasury_outstanding = 28.0

foreign_treasury_share = 0.32

foreign_treasury_stock = treasury_outstanding * foreign_treasury_share

print(f"GCC SWF USD exposure (midpoint): ${gcc_usd_exposure_mid:.2f}T")

print(f"Foreign Treasury stock: ${foreign_treasury_stock:.2f}T")GCC SWF USD exposure (midpoint): $2.53T

Foreign Treasury stock: $8.96TThat is the mechanism most commentary skips. Gulf capital is not a footnote to US financial markets. It is embedded in the cap table of the only sectors still treated as plausible US growth stories: technology, infrastructure, data centers, platform equity, commercial real estate, and a large share of long-duration risk capital. If the security guarantee breaks, the portfolio question changes with it. What looked like normal reserve recycling starts to look like concentrated geopolitical exposure.

Investor exposure by AUM and USD share. Gulf SWFs matter not because they are the only exposed actors, but because they are large enough to turn political realignment into market structure.

This is the financial-elite network layer. States act through portfolios. Sovereign wealth funds, family offices, university endowments, venture allocators, pension funds, and private-equity sponsors do not sit in separate universes. They co-own the same asset stack. Once the geopolitical premise behind that stack changes, the reallocation mechanism is already sitting there waiting.

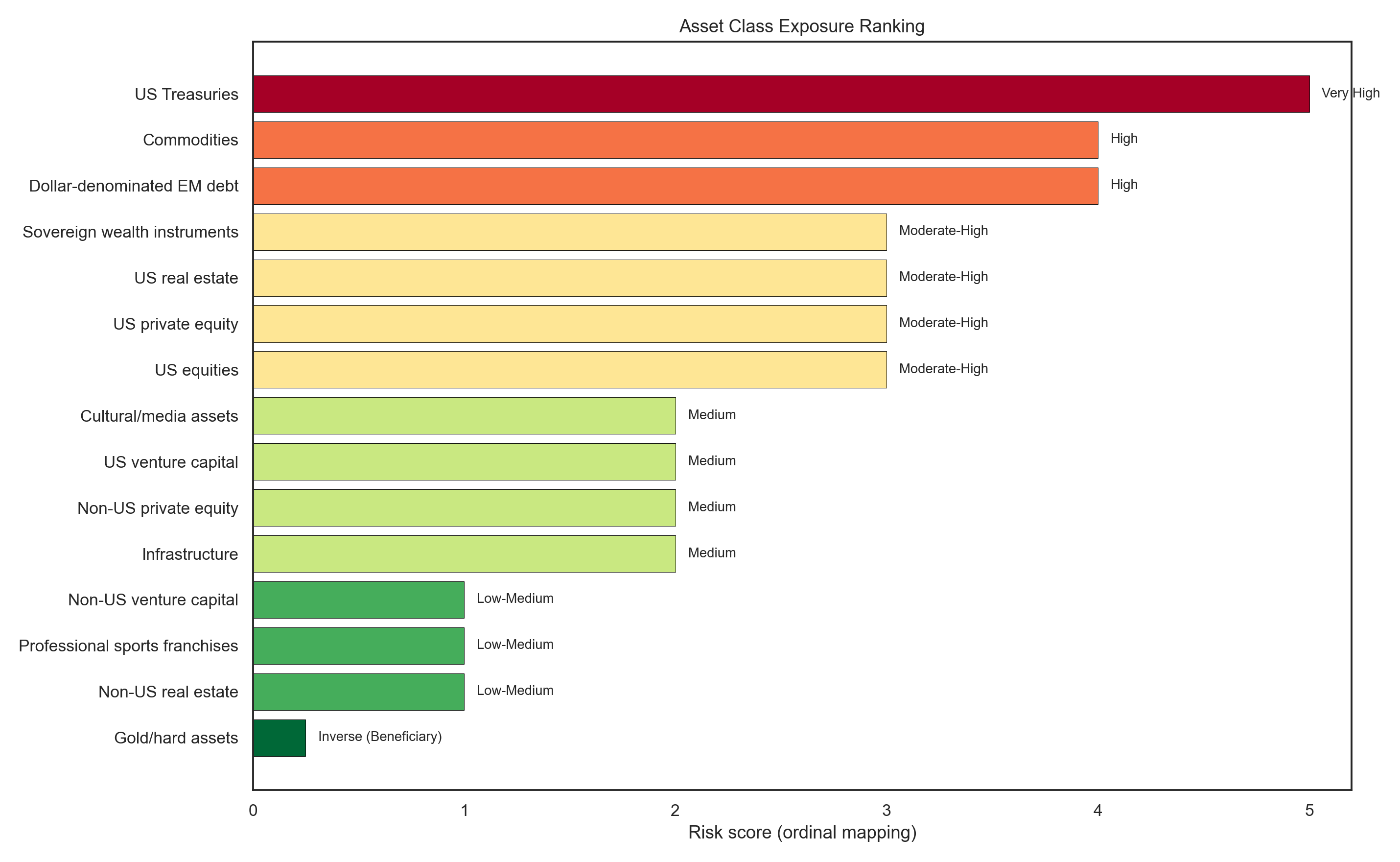

Step 4: Identify Which Asset Classes Break First

The asset ranking translates macro fracture into balance-sheet sequence. It matters because it clarifies sequence. Treasuries do not sit at the top because someone expects an overnight reserve apocalypse. They sit there because every other large-duration price in the system inherits from them. If foreign reserve demand softens, Treasury yields rise. If Treasury yields rise, leveraged private equity, real estate, infrastructure, and long-duration tech valuations all reprice on worse terms. That is not ideology. It is discount-rate plumbing.

Asset-class exposure ranking. The US balance sheet is vulnerable not only where the dollar is explicit, but where Treasury pricing quietly sets the floor under everything else.

The later war overlay sharpens this further. A Hormuz crisis is not just an oil shock. It is an energy shock, a fertiliser shock, an inflation shock, and a capital-allocation shock at the same time. If the same event also accelerates Gulf political rupture, then the most exposed asset classes are hit by both sides of the vice: worse macro inputs and weaker external capital support.

What the Pre-War Framework Actually Told Us

The pre-war framework already contained the essential argument.

It said the slow-fragmentation base case was only one path. It also said the shock-fragmentation scenario existed, and that the most exposed geography was the GCC precisely because currency pegs, reserve concentration, SWIFT dependence, and legal-financial exposure all run through the same node. Once you place the US on that same map under a collapse-exposure lens, the missing piece falls into place: the US is not outside the de-dollarization story. It is the most concentrated object inside it.

That is why the war matters analytically. It does not create the structure. It changes the speed variable. A framework built before the war can separate structural exposure from war-specific adrenaline. Then, once the war begins, you can ask the real question: which assumptions just moved from years to months?

The answer, in this framework, is Gulf recycling.

If the security bargain that made GCC dollar recycling rational is publicly damaged, then sovereign wealth reallocation is no longer just a portfolio optimisation problem. It becomes a regime-survival problem for the states involved. That is the ceiling on escalation. Not because markets are morally superior to war, but because the same people underwriting the US capital stack are also the people whose political incentives would change fastest under security rupture.

Be specific about what "underwriting" means. Gulf sovereign wealth isn't parked in index funds. It is load-bearing infrastructure in the only sectors the US still treats as credible growth stories: venture capital, data centers, commercial real estate, media consolidation, tech equity. The AI buildout that represents the last broadly accepted US economic thesis depends on two inputs simultaneously — cheap energy and Gulf capital deployment. A war that threatens both at once isn't a risk to sentiment. It is a structural threat to the growth model itself.

That is why the ceiling on US escalation is financial, not military. Every escalation option — from Hormuz blockade-running to strikes on Iranian territory launched from Gulf soil — accelerates the economic collapse the US is simultaneously trying to prevent. Oil at $200, fertiliser offline, job creation already negative before the war started, the entire AI bet premised on cheap energy now under direct threat — and then add a Gulf capital liquidation event on top. The US financial system does not survive that sequence intact.

Iran identified this correctly. The Hormuz closure and the economic warfare dimension are not a separate front from the military campaign. They are the same operation. Force the US into a position where the financial architecture it depends on becomes the weapon used against it. The pre-war exposure map is exactly the terrain being exploited — every channel this framework flagged as concentrated is now a pressure point under active stress.

And the speed variable is not just about markets. Gulf governments facing domestic populations watching their territory absorb strikes from US-adjacent operations do not have the luxury of a slow reallocation timeline. Portfolio optimisation logic gives way to political survival logic. The compression from years to months is not a market dynamic. It is a regime dynamic.

Which brings us to the endgame the framework points toward but cannot price: Pakistan's historical nuclear guarantee with Saudi Arabia. If GCC states conclude the US security guarantee is void — and every signal since the war started, from Qatar's "all options are open" to the UAE's public capital signaling, says they are reaching that conclusion — then the rational move is to activate an alternative security architecture. Pakistan's nuclear umbrella, extended to Saudi Arabia and potentially Turkey, changes the regional calculus permanently.

For Israel's war objectives at any level, a nuclear-armed GCC security architecture makes escalation dominance functionally unachievable. The deterrence calculus shifts not just for this conflict but for the regional order that follows it. For US influence, it means the security-for-recycling bargain — the foundation the dollar system's Gulf node rests on — comes permanently unbundled. That is not a temporary political rupture. It is the security architecture and the financial architecture decoupling simultaneously, with no mechanism to re-couple them.

The sovereignty calculus driving this is the same one reshaping African state behaviour: when alignment with the United States demonstrably does not mean the United States will account for your interests, the rational response is to build your own architecture. The GCC is learning the same lesson the African Union is learning, at higher stakes and faster speed. The difference is that the GCC holds the capital positions that make the lesson existential for the US, not just for the states doing the learning.